The Chilean Forestry Sector and associated risksAGRICULTURAL

Fernando Raga. Forest Development Manager of CMPC (Paper and Cardboard Manufacturing Company), Director of the Forestry Institute (INFOR) and Second Vice-President of the Timber Corporation

Wood is the raw material that is most consumed in the world, with a consumption rate that is triple that of cement, four times that of steel and twenty times that of plastic. It would be almost impossible to replace wood with any other material, not only because of the enormous volume consumed each day in the world, but because of the vast environmental costs involved, such as increased energy consumption and greater pollution levels, generated within the production process itself and by the way such a material would be used. Moreover any substitute would most likely come from non-renewable sources. Highly productive cultivated forests are an eco-efficient solution to the world’s current and future timber needs. Chile has based its forestry sector on these types of forest; here, we take a look at the industry’s main figures, its production cycle and the main associated risks.

The World’s Forests

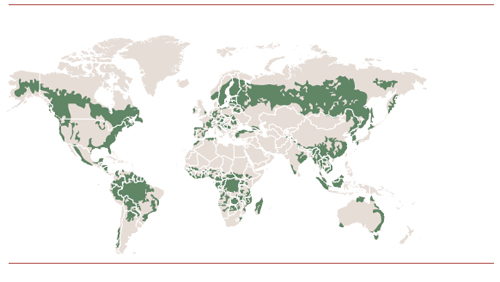

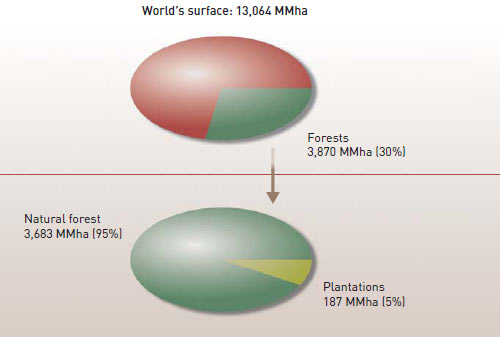

According to the FAO (Food and Agriculture Organisation of the United Nations), there are 3.87 billion hectares of forest in the world, covering 30% of the continental surface of the planet. Of this 30%, 187 million hectares are forest plantations (less than 5%), 47% of which are destined for industrial use, whilst the remaining 53% consists of reforested land.

The FAO estimates that approximately 25 million hectares contain rapid growth plantations, constituting 13% of the world’s total plantations and 0.6 % of its total forest area.

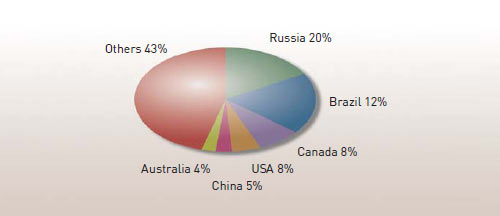

The countries with the largest areas of forest are Russia, Brazil, Canada, USA, China and Australia, in that order. All together are home to 57.2% of the world’s forests. Chile has only 0.41% of the world’s forests and 1.87% of the forests in Latin America and the Caribbean.

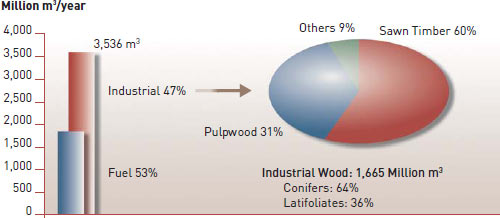

3,536 million m3 of wood is produced in the world, most of which is used for fuel (53%) or industrial purposes.

Wood used in industry can be further subdivided into pulpwood and sawn timber (depending on whether the material is more apt for cellulose or solid wood), with 31% and 60% consumed for these purposes, respectively.

Map of the world’s forests

In 2000, 35% of the world’s industrial demand for wood was supplied from forest plantations and this figure is expected to rise to 40% by 2020.

The Forestry Sector in Chile

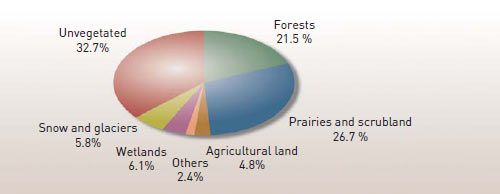

Continental Chile is situated in the southern hemisphere, to the West of Argentina and to the South of Peru. It has a surface area of 76 million hectares and a population of more than 16 million. Forests currently occupy 21.5% of Chile’s surface, equivalent to 16.2 million hectares.

Chile’s forestry resources consist of 16 million hectares of forest, 86% of which corresponds to natural forests and 14% to plantations. The main planted species are the Radiata Pine (64% of the plantations), the Eucalyptus Globulus and the Eucalyptus Nitens. These three species cover 92% of the total planted surface. Over the last 33 years, the annual plantation rate has exceeded 100 thousand ha/year, far above the felling rate. The plantation of eucalyptus trees in Chile increased significantly during the 1990s; indeed, more eucalyptus trees are planted today than Radiata Pines.

Among Chile’s competitive advantages are the cycles and yields obtained from pine and eucalyptus trees on the world market. Chile has the third highest growth rate for eucalyptus yields, after Brazil and Argentina, with cycles of 10 to 12 years and yields of 25 to 40 m3/ha/year, depending on the species. In effect, the Chilean Radiata Pine competes with the best yield rates in the region and is only surpassed by some subtropical species of Argentina and Brazil, with average yields of 23 m3/ha/year and cycles of 18 to 25 years.

Chile and Uruguay are the only countries in Latin America to experience net growth in their forest covers, thanks to high plantation rates.

Much of the country’s land, which had suffered from erosion and degradation in the past due to agricultural practices, has since been reforested. As a result, some 1.76 million hectares have been recovered, equivalent to 84% of the planted land. These hectares can capture almost 40 million tonnes of CO2, helping to reduce the Earth’s greenhouse gases.

2,075 thousand hectares of Chile’s forests have been approved and certified according to PEFC (Programme for the Endorsement of Forest Certification) or FSC (Forest Stewardship Council) sustainable forest management standards. These hectares correspond to approximately 75% of the country’s plantations.

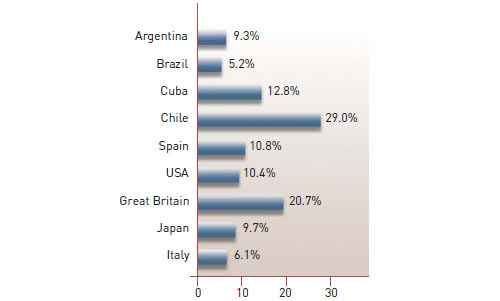

The country has 13.4 million ha of native forest (equivalent to the combined surface area of South Korea and Taiwan). 19% of national territory and 29% of the forests is under the protection of the Chilean State, through National Parks, National Reservations and Natural Monuments; indeed, Chile is one of the countries with the highest percentage of protected forest in the world. Neither should we forget that there are 2 million hectares of protected forest in private properties, equalling 14.6% of the country’s total protected forest.

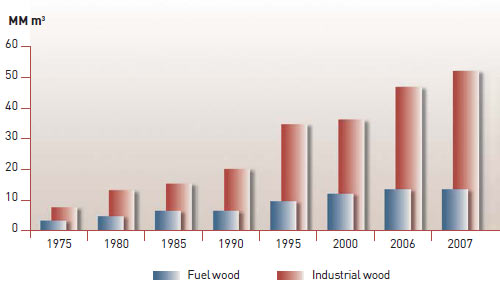

In 2007, the annual timber harvest reached 52 million m3, of which 38 million m3 was used for industrial purposes and 14 million m3 for energy. Of the wood used in industry, 98% comes from plantations, whereas 44% of that used for energy still comes from natural forests; the rest is from plantations and waste from primary and secondary industry.

40% of all industrial wood is used in sawmills, with a similar percentage used for pulpwood and paper. The rest is used to make boards, panels and other products. Many of these products are exported.

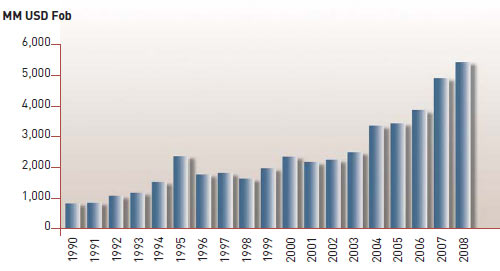

Forestry exports have risen continuously over the last few years, resulting in a positive trade balance. Exports in 2008 totalled USD 5,454 Million, representing a growth of approximately 16% over the last 6 years. Over this period, the export market has diversified, with the wood produced in Chile now reaching up to 115 countries.

The forestry sector is Chile’s second largest exporting industry, behind only large-scale mining. It generates direct and indirect employment for approximately 400 thousand people and represents approximately 7.3% of GDP. The industry’s products are exported to more than 115 countries, with China and the US being Chile’s main export markets, followed by Japan and Mexico, although the US market shrunk over the last year due to the international financial crisis.

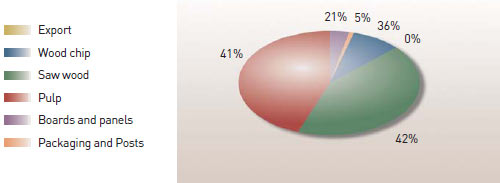

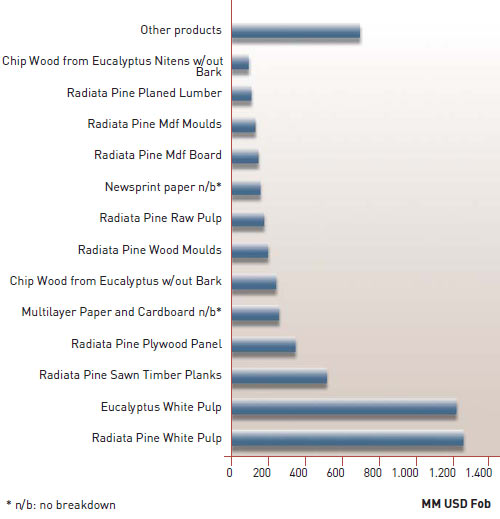

The main export products are white pine timber and eucalyptus pulp, followed by sawn timber.

The Chilean forestry sector is very concentrated, with two large companies dominating the market: Arauco and CMPC. Together, these companies account for nearly 72% of the export market and control 70% of the pine plantations and 40% of the eucalyptus plantations. The third largest company is Masisa, Latin America’s leading wood board producer.

Forest surface

Source: State of the World Forest. FAO, 2009 (data from 2005)

Forest land: main countries

Source: FAO 2005

Global wood consumption

Source: FAO 2008

Chile: land use distribution

Source: INFOR, Chilean Forestry Sector 2008

Proportion of protected forests

Annual Timber Felling

Source: Infor 2008

Chile: Main industrial uses of wood

Source: Infor 2008

The effects of the financial crisis

The international financial crisis has affected the subsectors of Chile’s forestry industry to varying degrees. In early 2008, the effects were already being felt as demand from the US, Chile’s main solid wood export market, dropped. In May 2008, house starts dropped by 45.2% from May 2009 levels and by almost 80% from 2006 levels. Initially, only wood producing companies exporting to this market were affected; however, after the Lehman Brothers’ collapse, the contraction in demand spread to other markets, such as Europe, Asia and the Middle East, affecting, in turn, the demand for sawn timber. In 2008, 148 sawmills (mainly small and medium sized) were forced to close their businesses in Chile. In the last quarter of 2008, it was the cellulose industry’s turn, when international demand for Chile’s products practically seized up for more than four months, only to return weakened, with prices at which no plant in the Northern Hemisphere could have continued producing. However, the effects on industries such as paper and sanitary products were much less severe. In 2009, the largest companies were forced to reduce production in their sawmills and forest harvests, along with the rate of cellulose production. The decline in the sawmill sector now appears to have bottomed out and some improvements are expected for the 4th quarter of 2009. The volume of cellulose sales has increased thanks to greater demand from China, albeit at lower prices, with intermittent rises. It is hoped that the different subsectors of the industry will see improvements, as demand picks up and the process of recovery consolidates over the coming year.

Chilean forestry exports

Source: Chilean Forestry Statistics, Central Bank

Source: Infor 2008

Structure of forestry exports

Source: Infor 2009

Risks associated to the forestry business

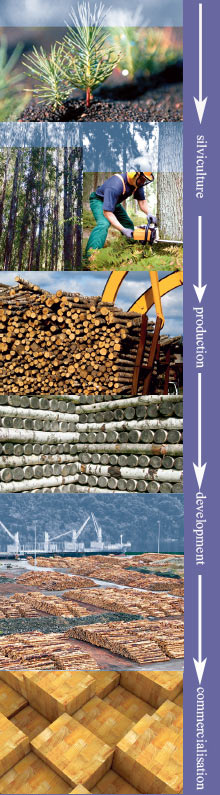

The economic cycle in forest plantations comprises four main stages:

- a. Silviculture: Silviculture covers plant production, management of forests (fertilisation, thinning out, pruning) and maintenance and care of trees until they are ready to be harvested. This is the longest stage of the forestry cycle, lasting between 10 and 25 years, depending on the species. The hazards to which forests are exposed during this stage consist of weather risks (windstorms, floods, snowstorms), biological risks (plagues), man-made risks (territorial occupation, theft of wood) and fire risks. The last factor is the most critical for the business and shall be discussed in further detail below.

- b. Forestry production: Forestry production covers the harvesting of forests and transportation of logs to development plants. The main hazards during this stage of the cycle are risks affecting the health and safety of the employees carrying out the work, the risk of faults and failures in the equipment used and risks related to safety/security during transportation.

- c. Wood engineering: This is the stage in which products such as sawn and remanufactured timber, fibre and plywood panels, cellulose and paper are industrialised. The principal hazards during this stage of the process are those normally associated to industries: fires and earthquakes (Chile is prone to high seismicity), faults and failures in the equipment, loss of profit and health and safety. Generally, these risks are no different from those found in any other industry.

- d. Commercialisation: This stage comprises the consignment of products to the internal market’s points of sale or to the ports for exportation. Considering that the bulk of national production is exported, the main risks in this stage are those normally associated to ocean freight shipments and are similar to those of any other large-volume non-perishable goods export process.

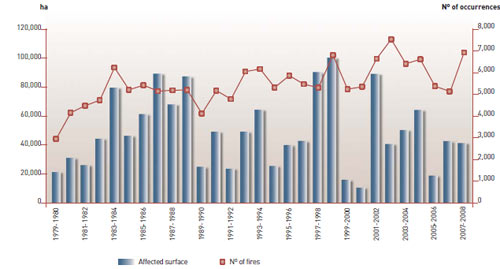

Annual Forest Fire Statistics

Forest fires

Rainfall levels in Chile’s forests fluctuate significantly throughout the year, although the strongest rainstorms occur in autumn and winter, whilst the summers are generally dry. Consequently, the forest fire hazard season is usually from November through to April of the following year, when fires can start and spread easily due to the spring and summer weather conditions. The most critical months are generally January and February. However, meteorological phenomena in the area, such as El Niño and La Niña, can make the season more severe or make it last longer.

Although there are approximately 5,200 fires each year affecting 52,000 hectares on average, the incidence and damage caused during each season fluctuate enormously.

The natural vegetation on prairies and in the scrublands usually sustains the most severe damage, followed by woodlands and forests. Commercial plantations, mainly Radiata Pine plantations, also suffer some damage, albeit to a lesser extent: an average of 7,000 hectares is affected each season. This number is high, but this 0.3 percentage of incidence poses no structural threat to the existing mass of 2.2 million hectares.

The estimated financial loss is approximately USD 50 Million per fire hazard season. However, apart from the loss of vegetation caused directly by the fires, there are other indirect effects and consequential losses resulting from the loss of vegetative cover, such as flash floods, landslides and desertification. There are also added social costs, such as the destruction of homes and, more importantly, the deaths of inhabitants and firefighters.

Most of the forest fires in Chile are caused by human activities, sometimes through negligence, sometimes by accident and sometimes intentional. Fires caused by lightning have also become more frequent over the last few years. Thanks to campaigns designed to raise awareness of the potential danger and damage of forest fires and to greater controls and general oversight, the use of fire in forest environments has declined over the last few years. However, the problem persists, especially with small landowners who continue to use fire carelessly.

88% of all the forest fires affect an area of less than 5 hectares. A few of these fires can spread to large proportions. However 0.6% of forest fires in Chile, representing approximately 40 fires over an area of more than 200 ha per season, can spread to cover more than 2,000, 6,000, 10,000 or more hectares each, concentrating fire-fighting resources, causing social alarm and damage and burning approximately 67% of the areas affected by forest fires in Chile.

In Chile an average of 7,000 ha of plantations suffer fires each year (0.3%), but this amount poses no structural threat to the existing mass of 2.2 Million Hectares.

Through the National Forest Corporation (CONAF), the Government of Chile implements preventive policies and deploys fire-fighting units, mainly in areas belonging to small and medium-sized landowners, in parks and national reserves and in lands owned by the state. The Government also regulates how fires may be used in rural environments. Approximately USD 7.5 Million are invested in this work every season.

At the same time, forestry companies invest some USD 20 Million each year in preventive work and fire fighting operations in their forests, as well as in those in adjacent lands belonging to other landowners.

FAO

http://www.fao.org/forestry/home/es/

PEFC

http://www.pefc.org/internet/html/